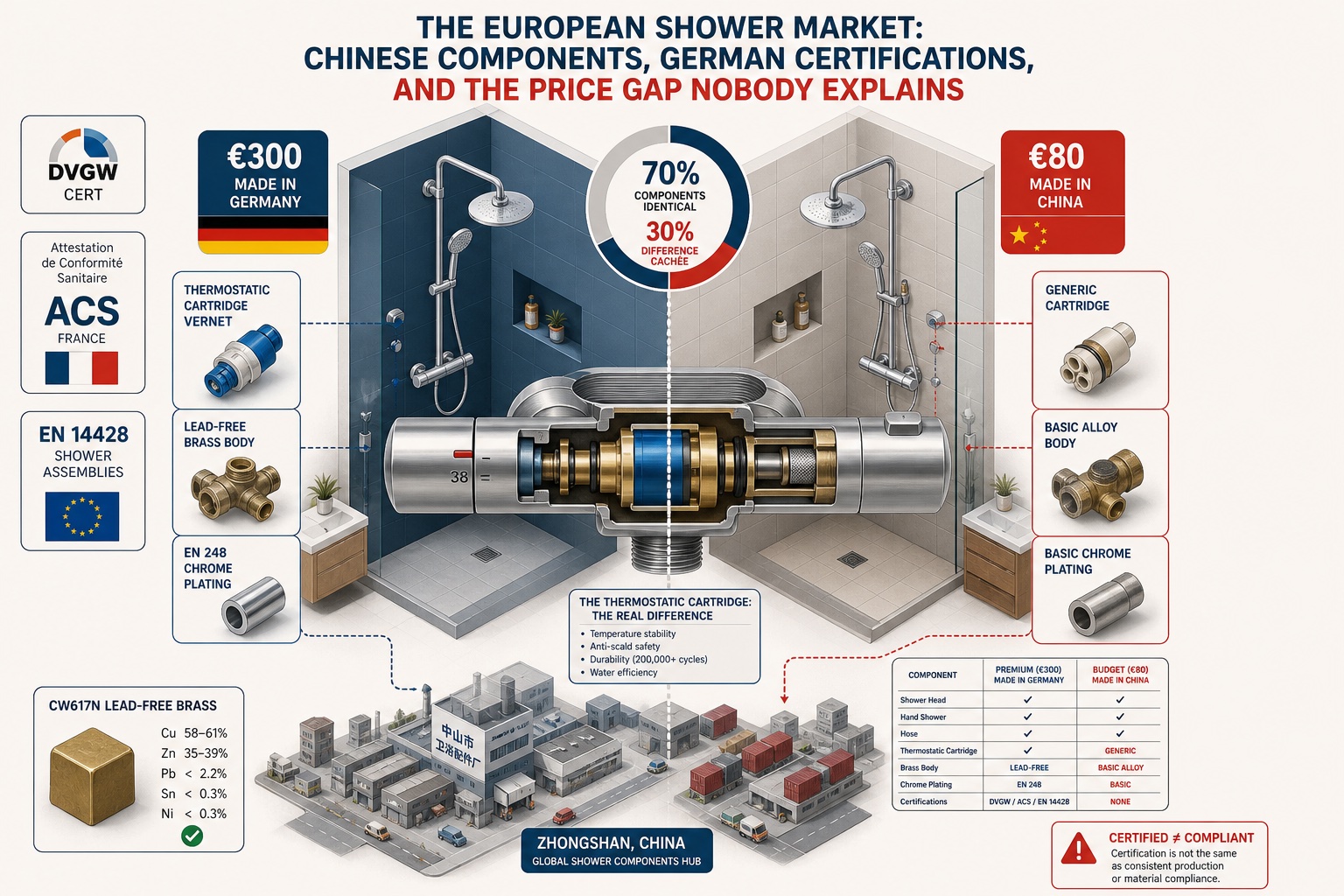

A €300 German-branded shower set and an €80 Chinese-branded one can share 70% of the same components by count. The remaining 30% — and the certification layer around them — is where the price gap is real. We map where shower products are actually made, what DVGW, ACS and EN 14428 verify, and which components inside the box determine five-year performance.

Walk into a large European DIY superstore — a Bauhaus in Stuttgart, a Brico Dépôt in Lyon, a Gamma in Rotterdam — and the shower section presents a price range that defies easy explanation. At one end, a complete shower system from a recognised German brand: overhead rain head, hand shower, slide bar, thermostatic mixer, hoses, and wall fittings, packaged in a box with precise engineering diagrams and a reassuring weight, retailing at €280 to €380. Three metres away, what appears to be the same configuration — superficially identical chrome finish, same rain head dimensions, same thermostatic promise on the packaging — under a brand you have not heard of, made in China, at €75 to €95.

The question that most buyers ask at that moment is the natural one: what exactly am I paying for at the expensive end? The answer — which requires understanding where bathroom products are actually made, what the certification marks mean and what they do not, and what genuinely distinguishes components at different quality tiers — is not the one that either the premium brand's marketing department or the budget product's importer has an incentive to explain clearly.

This is that explanation.

Where Showers Are Actually Made

The global production geography of bathroom fittings — showerheads, mixer taps, slide bars, shower enclosure hardware, thermostatic cartridges — is more geographically concentrated than most European buyers realise. The dominant manufacturing cluster is in Zhongshan City, Guangdong Province, supplemented by Foshan, Kaiping, and parts of Zhejiang Province for specific product categories.

Zhongshan's Guzhen district is known as the global capital of lighting. Its neighbour, the industrial zones around Xiaolan and the broader Zhongshan manufacturing belt, are the global capital of sanitary hardware. The concentration is not incidental — it reflects decades of supply chain development, tooling infrastructure, plating capacity, and specialist labour that have made the Pearl River Delta the most efficient place on earth to manufacture brass fittings, chrome-plated components, and stainless steel shower accessories.

The companies in this cluster produce for everyone. The same factories that supply components under their own export brands or generic labels for the low-price segment of the European market produce, under contract or OEM arrangements, for brands that European consumers associate with German or Austrian engineering heritage. This is not a secret in the industry. It is simply not something that brand marketing communicates, for understandable commercial reasons.

The proportion of finished shower products sold in Europe that contain Chinese-manufactured components — whether those products are branded Chinese, European-designed-Chinese-made, or simply assembled in Europe from Asian parts — is very high. A credible industry estimate, consistent with MAXAM's sourcing experience across this category, is that over 80% of complete shower systems sold in European mid-market retail carry Chinese-origin components in the majority of their component count, regardless of the brand on the box or the flag on the packaging.

What "Made in Germany" or "Engineered in Germany" actually means. For a shower product to carry a "Made in Germany" designation under EU origin rules, it must undergo its last substantial transformation in Germany — which, for assembled products, means the assembly that creates the finished article must occur in Germany. The components that are assembled can be sourced globally; the assembly step is what confers the origin designation. German brands that maintain German assembly operations are not misrepresenting their origin. The mixer cartridge installed during that assembly may have been manufactured in Zhongshan. Both things are true simultaneously.

"Engineered in Germany" carries no defined legal standard. It communicates that design and engineering specification work was performed in Germany — which may mean a detailed product development process with German quality engineers defining component specifications, tolerance requirements, and performance criteria, or it may mean a more limited design adaptation of a supplier's existing tooling. The phrase appears on products across the quality spectrum.

None of this means German-branded shower products are not superior to unbranded Chinese alternatives. The engineering quality, specification rigour, and ongoing supplier qualification that genuine premium brands apply to their component sourcing represent real value. The point is that the geographic origin story is more complicated than the packaging implies.

The Certification Framework: Four Standards, Four Different Answers

EN 14428: structural performance, not everything. EN 14428 is the European standard for shower enclosures — cubicles, screens, trays, and doors. It covers the strength and stability of the enclosure under load, the behaviour of glazing under impact, the water-tightness of seals, the corrosion resistance of frames and hardware in wet environment conditions, and dimensional tolerances. A CE-marked shower enclosure has been assessed against EN 14428.

The standard is meaningful for what it covers — particularly glazing safety (EN 14428 requires tempered or laminated safety glass) and long-term performance under wet conditions. What it does not address is the qualitative difference between a frame made from 1.2mm wall-thickness aluminium profile and one made from 1.6mm profile, or the difference between a roller mechanism designed for 30,000 opening cycles and one designed for 100,000. Products at opposite ends of the price spectrum can both carry CE marking under EN 14428 while delivering materially different long-term performance.

DVGW: the German standard that actually matters for water fittings. The Deutschen Vereinigung des Gas- und Wasserfaches (DVGW) is Germany's technical and scientific association for gas and water, and its W 270 and W 534 standards for products in contact with drinking water are the most demanding and commercially significant certification requirements in the European bathroom fittings market.

DVGW W 270 covers microbiological growth on materials in contact with drinking water — it requires that certified materials do not promote the growth of microorganisms beyond baseline levels. DVGW W 534 covers shower fittings specifically, addressing material requirements, construction requirements, and the thermal disinfection performance of thermostatic fittings (the requirement that a thermostatic shower valve can be set to deliver 60°C water for thermal disinfection of Legionella).

In the German market — Europe's largest bathroom fittings market by value — DVGW certification is effectively a commercial requirement for products sold into professional specification channels. It is not legally mandatory for consumer retail sales, but its absence from a product targeting professional installation creates a credibility gap that is difficult to overcome commercially in Germany and increasingly in German-influenced markets such as Austria, Switzerland, and the Netherlands. DVGW certification requires ongoing batch testing — not merely a type approval — and certified products can be subject to market surveillance testing. The certification body fees and testing costs are substantial, which is one reason why products in the lower price segment do not carry it.

ACS: the French Attestation of Sanitary Conformity. The French Attestation de Conformité Sanitaire (ACS) is the equivalent framework in France for materials in contact with drinking water. Unlike DVGW, ACS is a regulatory requirement in France — products in contact with drinking water intended for permanent installation in French buildings must carry ACS attestation or demonstrate compliance with an equivalent recognised standard.

ACS testing covers chemical migration from materials into water — plastics, elastomers, lubricants, solders, brazing alloys — and microbiological aspects. In the consumer retail channel, ACS enforcement is less consistent than in the professional channel. The gap between regulatory requirement and retail market practice is one that enforcement is gradually closing, but it remains a significant one. ACS is not available for products that cannot pass the chemical migration testing, which excludes products using lower-grade plastic compounds, non-compliant elastomers, or lead-containing brass alloys — a quality criterion that eliminates a segment of lower-grade Chinese brass fittings from French market eligibility.

KTW and WRAS: the broader European picture. Beyond DVGW and ACS, the landscape includes KTW (Germany's plastics-in-drinking-water guideline), WRAS (the UK Water Regulations Advisory Scheme), and the long-delayed European harmonised standard for construction products in contact with drinking water, which has been under development since the 2000s and has not yet produced a fully operative EU-wide framework.

The absence of a single harmonised EU drinking water contact standard is commercially significant. It means that compliance must be demonstrated market by market against national technical standards rather than against a single EU certification. A product that has invested in DVGW certification is well-positioned for Germany, Austria, Switzerland, and the Netherlands. It may still need ACS certification for France and KTW assessment for broader German market channels. The multi-standard compliance requirement adds cost and complexity that is disproportionate for smaller importers or lower-price products, contributing to the market structure where certified products cluster in the upper price tiers.

The Component Inside the Component: Where the Real Quality Differences Live

The thermostatic cartridge: the most important part nobody sees. The thermostatic cartridge is the engineering heart of a thermostatic shower mixer. It is the component that maintains water temperature within ±1 or ±2°C of the set point regardless of fluctuations in the hot and cold water supply pressures — the component that makes a thermostatic shower work as claimed and that distinguishes a thermostatic shower from a pressure-balance valve or a manual mixer.

Thermostatic cartridges use a thermostatic element — typically a wax capsule or a bimetallic element — that expands or contracts with temperature changes, mechanically adjusting the hot/cold mix ratio. The performance characteristics that matter — temperature stability range, response speed, maximum temperature anti-scald protection, durability over a claimed cycle life — depend almost entirely on the quality of this cartridge.

The dominant global suppliers of thermostatic cartridges are a small number of specialist manufacturers. Vernet, a French company, and Flühs Drehtechnik, a German company, are the benchmark suppliers for European premium specification. Their cartridges are used in products across a wide price range — including in products that carry the major German and Swiss brand names — and they are also available as OEM components to Chinese manufacturers producing for the European market.

At the lower quality tier, thermostatic cartridges are produced by Chinese manufacturers in Wenzhou and the Pearl River Delta at a fraction of the cost. The temperature stability performance, cycle life, and anti-scald reliability of these cartridges is, in laboratory testing, demonstrably lower than the premium alternatives. The gap between a 50,000-cycle rated cartridge and a 200,000-cycle rated one is invisible in a retail shower, apparent to a professional installer, and significant over a product's operational lifetime in a household.

This creates a specific category of misrepresentation risk in the market. A thermostatic shower branded with German certification marks may carry a Vernet or Flühs cartridge — the certification marks are an accurate representation of product quality. Or it may carry a Chinese-produced cartridge that meets minimum certification requirements but operates at the lower end of performance — in which case the certification marks are technically accurate but do not distinguish the product from significantly better alternatives. The certification mark is on the assembled product, not on the cartridge, and the cartridge is not visible without disassembly.

Brass alloy composition and lead content. Shower mixer bodies, connection fittings, and hand shower bodies are typically manufactured from brass — an alloy of copper and zinc with varying minor element additions. The composition of the brass matters: lead content in particular affects both machineability (higher lead content makes the alloy easier to machine) and, critically, lead leaching into drinking water.

Conventional free-machining brass contains 2–3% lead by weight, which historically made it the default choice for sanitary fittings. The regulatory picture for lead in drinking water contact materials has tightened progressively across the EU, the US (where the Safe Drinking Water Act lead-free standard of 0.25% weighted average lead content has been in force since 2014), and the UK. European market surveillance has found non-compliant lead leaching from imported shower components — an issue that affects Chinese-origin products at the lower end of the quality range but is not exclusive to them.

Low-lead or lead-free brass alloys — including silicon brass (CW724R in the EU material classification) and bismuth brass alternatives — have become the standard for premium-specification products and for products certified under ACS, DVGW, and WRAS. The alloy cost is higher and the machinability more demanding, requiring tighter process control at the casting and machining stage. For importers sourcing shower fittings from China, the brass alloy specification in supplier contracts matters. A contract that specifies "brass body" without specifying alloy composition or lead content limits is a contract that does not guarantee compliance with current and upcoming European regulatory requirements. Material test certificates for brass composition — verifiable by X-ray fluorescence analysis — are a minimum requirement for any serious quality programme in this product category.

Surface finishing: why chrome looks the same and isn't. Chrome plating on shower components is a multi-layer process: typically a copper base layer, a nickel intermediate layer, and a chromium top layer, applied by electroplating. The cosmetic result — a reflective, corrosion-resistant surface — can look identical across products at radically different quality and price levels. The durability is not identical.

EN 248 is the European standard for decorative chrome plating on sanitary fittings, specifying corrosion resistance requirements in terms of CASS (copper accelerated acetic acid salt spray) testing hours. An EN 248 test to 192 hours of CASS corresponds to an expected outdoor exposure of approximately 30 years; for indoor sanitary use, this is a demanding benchmark.

The plating thickness, layer adhesion, and substrate preparation quality that determine CASS performance are not visible to the consumer. A shower component at €25 FOB and one at €55 FOB can be visually indistinguishable at point of sale and diverge significantly in resistance to corrosion after five years in a humid bathroom environment. The rust spots that appear around the seal rings or on the slider mechanism of a budget shower rail after two or three years of use are almost always a chrome plating durability failure, not a structural failure. The correlation between chrome plating quality and product price is real but imperfect: some Chinese manufacturers producing for European premium brands maintain CASS testing in their own quality programmes and achieve EN 248 compliance consistently. Others — particularly at the lower price tiers — do not test to this standard.

The Price Anatomy: What the Premium Buys, and What It Doesn't

A complete shower set — thermostatic mixer, overhead shower head (typically 250–300mm diameter rain format), hand shower, 1.5m flexible hose, slide bar, and wall outlet elbow — occupies a retail price range in European DIY and plumbing merchant channels from approximately €75 (unbranded Chinese import, no certifications) to €800 or above (major German or Swiss brand, premium specification, full certification package). The mid-market range, where the bulk of units are sold, sits between €120 and €380.

Decomposing this range reveals a distribution across several value drivers that are unevenly represented in marketing communications.

Brand and distribution margin accounts for a larger share of the premium tier's price differential than most buyers would expect. The cost of maintaining a European sales organisation, trade marketing investment, professional channel support (installation instructions, technical hotlines, replacement parts availability), and brand advertising is substantial. These are real costs, and the professional buyer who needs technical support when a mixer fails in a commercial installation is paying — legitimately — for the infrastructure to receive it. The DIY consumer replacing a shower in a domestic bathroom may not need most of this infrastructure.

Certification costs are a real component of premium pricing but are more modest in impact than the value they represent. DVGW certification for a mixer valve involves testing fees of several thousand euros and ongoing surveillance costs spread across production volumes. For a product selling 50,000 units per year in Germany, this is a per-unit increment in the range of €0.10–0.30. The certification's value — in terms of product liability protection, market access, and consumer trust — is disproportionate to its cost component. Certifications are cheaper than they look from the outside.

Thermostatic cartridge quality is a genuine and meaningful price driver in the thermostatic mixer segment. The cost difference between a Vernet or Flühs cartridge and a comparable Chinese-produced alternative can be €8–15 per unit at the component level — a difference that represents a meaningful portion of the FOB price differential between equivalent-specification premium and mid-market products.

Brass alloy quality contributes a smaller but real differential: low-lead silicon brass costs approximately 15–25% more than conventional free-machining brass at the casting stage. **Chrome plating quality** (measured in CASS hours) contributes a cost differential at the component level that is often €3–8 per unit for a complete set of plated components.

Genuine design and engineering work — products with proprietary shower head flow geometries, precision-engineered spray patterns, ergonomic hand shower designs, or thoughtfully designed installation systems — represent a category of premium that is genuinely difficult to replicate at lower price points. This is the quality dimension most underappreciated by consumers who assume the premium is primarily brand and margin.

A €300 German-branded shower set and an €80 Chinese-branded one can and do share 70% of the same components by count — the chrome-plated slide bar, the hose fittings, the wall mounting plates, and various plastic and rubber seals may come from the same Zhongshan factories. The remaining 30% — the thermostatic cartridge, the mixer body material and casting quality, the overhead shower flow plate, the key plated components — represent the meaningful quality differentiation, and these are the components that determine long-term performance rather than initial function. Both may work identically on day one. A five-year performance horizon is where the component quality differences manifest: in the temperature stability of the thermostatic control, in the cosmetic condition of the chrome finish, in the smooth operation of the slider mechanism, and in the absence of drips around the connections.

What This Means for European Importers

European companies importing shower products from China — whether for own-brand retail, white-label distribution, or supply into specification channels — operate in a product liability environment that requires more than a test certificate. The EU General Product Safety Regulation (GPSR), replacing the General Product Safety Directive from December 2024, imposes obligations on economic operators to maintain technical documentation demonstrating product safety conformity — documentation that goes beyond the CE declaration to include testing records, production surveillance, and a systematic risk assessment.

For shower products specifically, the questions that a responsible importer needs to be able to answer include: what is the brass alloy composition of the mixer body and what is the lead leaching result at the specified test conditions? What is the thermostatic cartridge specification and what is its rated cycle life? What CASS testing has been conducted on the chrome plating and what are the results? What EN 14428 assessment exists for the enclosure and which notified body conducted it? Answers to these questions cannot be inferred from the CE marking. They require a technical file that a competent supplier maintains and can produce on request, and an importer relationship that includes access to that technical file.

In MAXAM's experience sourcing bathroom products for European clients, the proportion of Chinese shower suppliers who maintain complete technical files consistent with EU economic operator requirements — as opposed to maintaining a set of certificates that satisfy a procurement checklist — is substantially lower than the proportion who can produce CE declarations on request. The gap between certification and documentation quality is, if anything, wider in bathroom products than in many other consumer categories, because the market has grown rapidly through retail and online channels where compliance scrutiny has been lighter than in the professional specification market.

The EU Construction Products Regulation revision and the GPSR's strengthened economic operator requirements are combining to raise the documentation and traceability expectations for construction product categories including bathroom fittings. The delegated acts under the revised CPR are expected to specify more granular performance declaration requirements for products in contact with drinking water, potentially creating a more harmonised framework than the current patchwork of national technical standards. For importers currently operating in the lower and mid-market shower segment with CE declarations that satisfy current market surveillance levels, the direction of travel is toward more rigorous documentation requirements and more systematic market surveillance.

The Buyer's Practical Guide: Navigating the Price-Quality Spectrum

For professional specifiers — architects, contractors, building developers, facilities managers — the practical guide to the European shower market is relatively clear: specify products with DVGW W 534 certification (for thermostatic mixers), EN 14428 compliance (for enclosures), and ACS attestation where French market supply is involved. These certifications, held genuinely by the supplying manufacturer and not merely by a parent brand, provide a defensible technical basis for product selection and a meaningful indication of quality commitment.

The thermostatic cartridge supplier should be identified in the technical specification where possible. Specifying "Vernet or Flühs cartridge" is a legitimate technical specification in professional channel procurement for thermostatic mixers, and suppliers who cannot demonstrate compliance with this specification should be evaluated carefully.

For consumer retail importers assessing own-brand shower product sourcing, the minimum viable qualification programme includes: brass alloy test certification with lead content verification, CASS testing results for chrome plated components, thermostatic cartridge cycle life data, and a current test report to the relevant EN standards from an accredited European testing laboratory (not a Chinese laboratory with unverifiable accreditation equivalence).

A complete shower system — thermostatic mixer with DVGW W 534 and ACS certification carrying a European-brand cartridge, EN 14428-compliant enclosure with genuine safety glass, chrome-plated components tested to EN 248 192-hour CASS — has a minimum realistic FOB price, at current Chinese manufacturing costs, that makes retail pricing below approximately €160 to €180 for the complete system commercially implausible for a product that meets all these specifications genuinely. Products retailing at €80 to €120 for a thermostatic complete system are either not thermostatic in any meaningful sense, not certified under the standards their packaging implies, or are operating on margins that make the supply chain economics structurally fragile — conditions that should raise questions for any importer evaluating their product liability exposure.

The €300 premium product may contain some of the same components as the €80 alternative. It is also providing certifications that carry real value, engineering quality in the components that matter most, and a supply chain that can be documented to a standard that will survive regulatory scrutiny. The price gap is not entirely justified and contains real brand margin. It is also not a fiction: a meaningful proportion of the premium buys something real, and knowing which proportion is which is the value that informed sourcing provides.

The Component Behind the Brand

The European shower market is, in its component reality, a globally sourced market with a European certification layer that varies from genuinely rigorous to nominally present. The €220 difference between the top and bottom of the consumer market represents a mix of legitimate quality premium, certification investment, brand infrastructure value, and margin — in proportions that vary by product and by brand but that the packaging is not designed to help buyers decompose.

For European importers, the relevant question is not whether to source from China — the answer for most mid-market shower product categories is that there is no commercially viable alternative at scale. The question is what specification and certification standard their supply chain actually meets, as opposed to what their supplier's certificate library suggests, and whether the documentation behind the product is sufficient to support their obligations as an economic operator placing goods on the EU market.

The regulatory trajectory — more rigorous documentation requirements, more systematic market surveillance, stronger economic operator liability under the GPSR — is moving toward a market structure where the distinction between certified-in-name and certified-in-practice will be harder to sustain. The importers who have already built their supply chains around genuine compliance will find that this is not a burden but a competitive position. The ones who discover the gap when a market surveillance authority does are learning the lesson at a much higher cost.

The price gap between the German-branded shower and the Chinese-branded one is partially explained by brand and margin. The remainder is explained by the components you cannot see: the cartridge inside the mixer, the alloy in the body, the plating thickness on the slide bar. That remainder is worth understanding before placing the order.

Tags

Sources

DVGW — Water standards W 270 and W 534 scope and certification requirements (dvgw.de); ACS attestation framework — French Ministry of Health and ANSES (sante.gouv.fr); EN 14428 — Shower enclosures standard, CEN European Committee for Standardisation; EN 248 — Decorative chrome plating on sanitary fittings (CEN); EU General Product Safety Regulation 2023/988 (entering full application December 2024); Vernet Group — Thermostatic element product range (vernet.fr); Flühs Drehtechnik — Sanitary cartridge systems (fluehs.de); MAXAM Group — Bathroom product sourcing and supplier qualification programme; Global Water Intelligence — European drinking water materials regulation overview; Construction Products Regulation revision — European Commission legislative progress, 2023–2025.